It took me almost two years to restore my salary after founding a startup

One founder's journey of trying not to go broke whilst starting a startup

There are many things that founders must figure out early on: identifying a problem worth solving, validating hypotheses, assembling a team, and building and iterating the first product. However, one of the topics that are taboo and not often talked about is the aspect of personal finance.

Unless you are sitting on a pile of cash from a lucrative past career, company sale, or inheritance, going without a paycheck while figuring out your company is a real issue.

Startup failure rates are high, and surviving the first year is critical. But YOU need to survive as an individual first so that your company can survive.

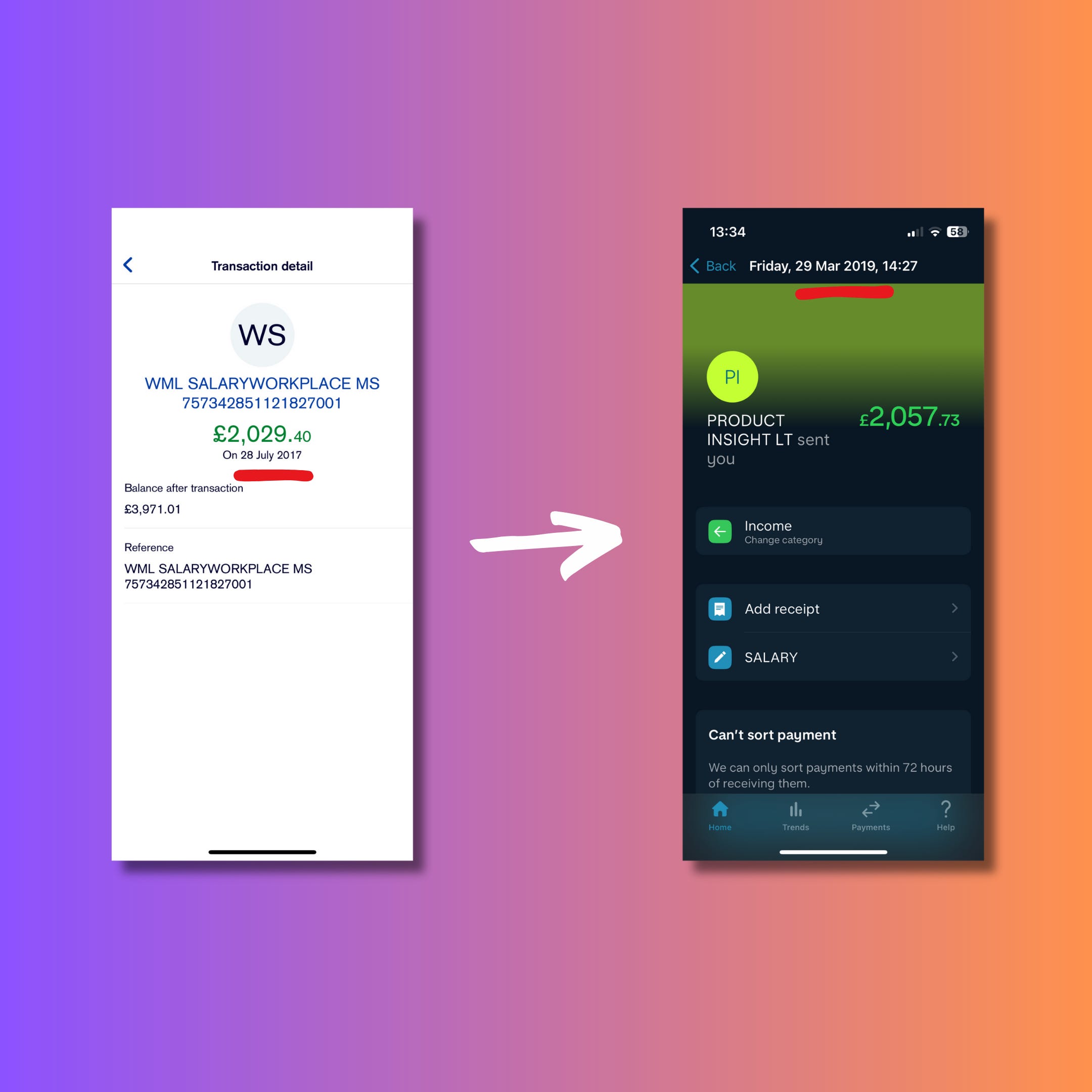

I recently wrote a post about the things I considered before quitting my job to start my startup Prodsight, and one of the common questions from readers was how I made it work without ending up on the street.

It took me nearly two years to restore my salary

I dug through my bank statements to determine the time gap between my last paycheck from the job and when I finally started making at least as much as I used to at my startup.

After starting my company, it took exactly one year and eight months to restore my salary. That’s nearly two years!

I was surprised, as it is way longer than I remember.

In this post, I will cover my steps to restore my personal finance equilibrium and all the sacrifices I made between 2017 and 2019.

Building up the savings nest

Before I quit my job, I built up a cache of savings to see me through the early days of Prodsight.

My target was to save at least six months’ worth of savings which I could tap into every month while I figure out ways of getting some capital into the business to draw a salary.

My wife and I always lived below our means, but I looked at all aspects of my spending to accelerate my savings rate and stretch it as far as possible in the “consumption” phase to see where I could make cuts.

Here are some of the things I’ve done to reduce monthly expenses:

Cut going out/drinking/eating out to a minimum

Worked from Starbucks, only buying their unlimited-refill filter coffee instead of renting office space

Made lunches at home instead of buying takeaways

Replace some meals with Huel (think protein-shake-like meal replacement)

Cooked dinner at home instead of going out

Cut any non-essential purchases like laptops, phones, or gadgets

Bought fewer new clothes and shoes

While I tried to keep these “cuts” focused on myself, it inevitably impacted my wife. She also had to make sacrifices and cover any shortfall in our household budget. I am forever grateful to her for this.

Putting our spare room on Airbnb

While the cost-cutting measures allowed me to reduce my “personal burn” rate significantly, there is only so much I could cut.

We also decided to rent our six-square-meter second bedroom to Airbnb guests to bring in some extra cash.

We met some wonderful people through this experience, but eventually, it started taking a toll on us, and we stopped Airbnb as soon as I started bringing in a salary again.

Taking on contract work

Reducing personal costs and dipping into savings made quitting my job and working on the startup possible, but it wasn’t a permanent solution.

Every month, my savings were dipping lower and lower, and all of the cost-cutting was starting to impact my quality of life. I had to start generating money from the company to pay myself.

Building a product that people are willing to pay for and for that to be enough to pay yourself a salary is not a small feat. It takes time to figure out which problems you want to solve. Designing and building software is a tedious process. You often get things wrong and must return to the drawing board. It was clear that I needed time to figure things out, and the quickest path was selling your labor.

A good friend Jamie McHale came to the rescue. He was running a technical consultancy, and one of his projects required a PHP developer. Mind you, I was a self-thought developer and barely qualified for the job, but luckily I could complete the coding tasks and got paid a decent daily rate for two days a week. This allowed me to earn enough money to cover my basic living costs and stop draining my savings. It felt like I froze time.

While my contract work was unrelated to my startup idea, it allowed me to spend the rest of my productive time figuring out my first product.

First product revenue

About three months after leaving my job, I launched my first mini-product/experiment called IntercomExport and started generating small amounts of revenue. It was a small app facilitating data exports from a popular customer service tool Intercom.

It was an experiment that enabled me to learn from a niche of users of Intercom about what additional needs I could solve for them. I identified that many of these users were exporting data from Intercom to analyze trends in customer requests. That finding ultimately led me to develop Prodsight.

I know I’m glossing over this part of the journey as I plan a more in-depth post on product discovery and iteration. I want to keep this post focused on the personal finance aspect.

Raising the first round

When I reached around $1,000 in Monthly Recurring Revenue (MRR) from my product experiments, I began looking for external investors to help me expand the team and continue growing the product.

The problem was - I didn’t know a single investor. This is not uncommon for early-career folks like me at the time, as you don’t just bump into high-net-worths while doing your office job.

Luckily, the local startup community came to the rescue, and various folks made warm introductions to local angel investors (shout out to Martin Lind, Calum Forsyth, and Gavin Dutch). I started taking meetings and pitching my startup. I had a vague idea of the whole process and took it one step at a time while allowing conversations with other founders and advice from blog posts to help me guide along the way.

As soon as the first angel investor said “yes,” the ball started rolling. I could leverage that first commitment and onboard some other angel investors. Once I had the critical mass, I began working on the legals and moving towards closing the round.

I closed our pre-seed round of investment in February 2019 - and that’s when I could start breathing a little easier and start thinking about paying myself again.

Deciding how much to pay myself

Deciding how much to pay yourself is a common dilemma for founders. Part of this is resolving your own conflict of interest. As an employee, you are continuously optimizing for maximum pay. However, as a founder and director, you must also protect the company’s interests, as maximizing your salary might harm the company.

The general rule for founders is to pay themselves enough for living expenses. As the company grows or raises investment, the founder’s salary increases until it eventually reaches the going market rate. Investors like to see founders making personal sacrifices and investing" sweat equity” into the business as a signal of their commitment to the startup.

I paid myself the bare minimum for the first 20 months, averaging around £1,000 monthly. It's not the kind of pay you can easily survive on, and far below what any outside person would accept to run the company. But that didn’t matter because I was betting on the company becoming a success one day. The equity I had in my startup was where I was banking my potential future returns.

As soon as we raised the first round of funding, my salary was determined by the new board of directors as part of the shareholder’s agreement. I proposed the number just above what I earned as a Product Manager. While I was underpaid, it was enough to live on, and I no longer had to stress about personal finances.

I could now entirely focus on building the company.

Special thanks to Martin Lind for reviewing a draft of this post.